Movie Equations: When everything is paramount

Paramount+ is here, and the theatrical window is not

The theatrical window is dead. Long live the theatrical window.

On February 24th, ViacomCBS became the latest company to announce it was approaching theatrical releases through the lens of a shortened window. Movies like A Quiet Place II and Mission Impossible 7 will play in theaters for 45 days before moving to the company’s new streaming service, Paramount+. Other movies might play for 30 days. Some, albeit seemingly increasingly more rare, will play the normal 90 days before moving to the streaming service.

ViacomCBS follows WarnerMedia and NBCUniversal in its move to radically upend the movie industry by effectively refusing to play by the rules that theater chains like AMC and Regal have enforced for years upon years. NBCUniversal struck a deal with AMC to pull movies after just 17 days in theaters, while WarnerMedia “got rid” of the theatrical window entirely, moving its 2021 slate to a “same day” release format, allowing movies to appear on HBO Max the same day they’re in theaters. Disney, a box office behemoth, is testing new formats, too.

What executives are trying to figure out is whether this will work out in the long run? One way to think about it is X representing time and Y representing steady revenue. If X (theatrical run, Pay 1) is shortened, then Y is immediately weakened. This is the short term approach. From a long term strategy, if A represents time (theatrical window, Pay 1), and B represents sustained monthly revenue, then shortening time (A) to boost sustained monthly revenue (b) could generate a sustainable form of revenue. The question is whether that’s better than the current options. Confusing? Let’s dig into it.

There are four areas we’ll explore in this thesis:

Total value of theatrical windows as they currently stand

Subscriber growth and incremental price increases over five years

Churn threats

Licensing versus exclusivity

To pull or not to pull?

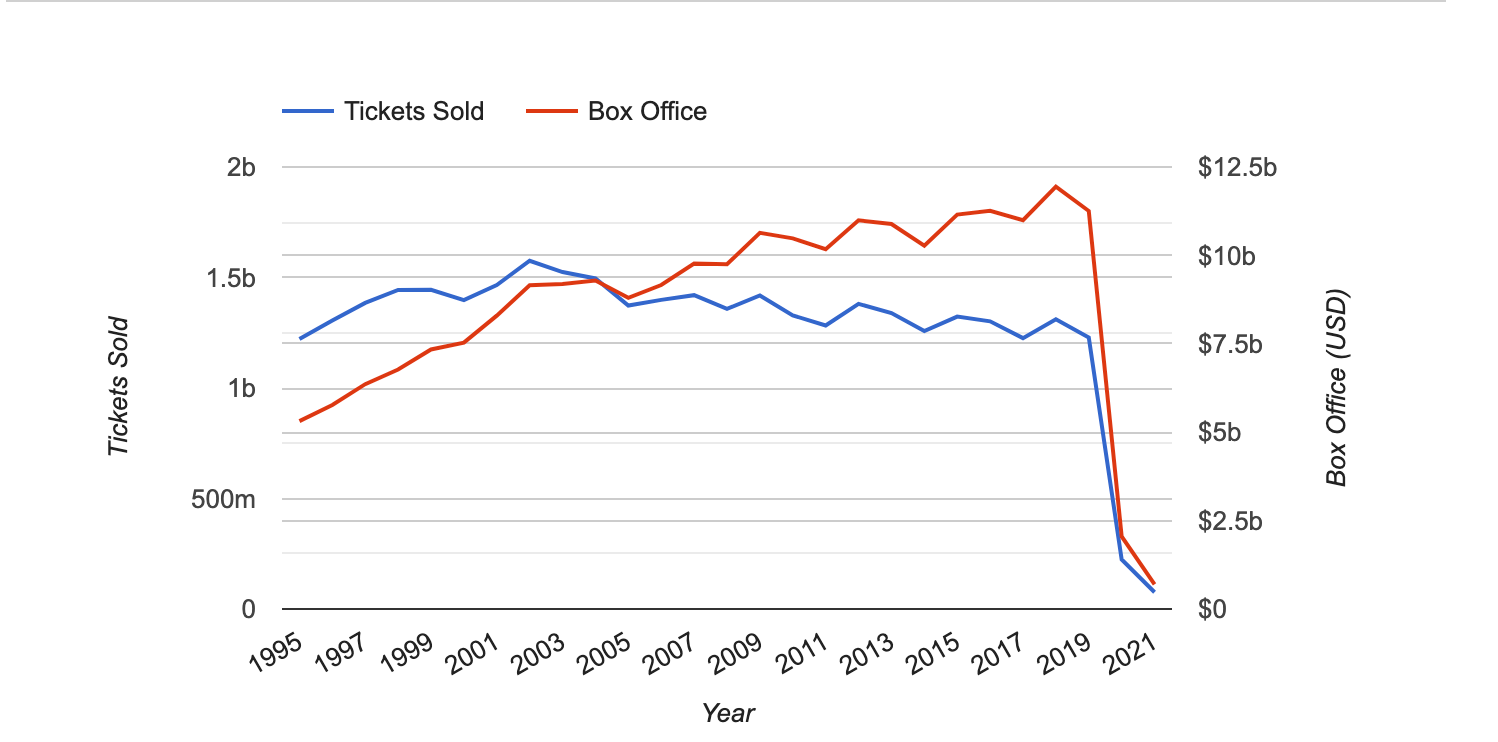

Numerous publications have written about the death of the theatrical window, but it was always an inevitability. The vast majority of a film’s revenue is made between the first and fourth week of its release. Some stragglers might find their way to a multiplex in the film’s fifth or sixth week, but statistically, once the fourth weekend passes, things dry up pretty quickly. Here’s just one example: Midsommar. Ari Aster’s film, which benefitted from word of mouth, earned just under $30,000 domestically after 85 days in theaters. It grossed roughly 93% of its total box office run within the first 31 days.

But studios like Paramount, Universal, Warner Bros., and Disney also want to use their theatrical partners to keep movies in theaters for 90 days for films where that revenue growth is vital. For example, Avengers: Endgame. While Midsommar earned another $3 thousand in theaters in its final 55 days, Endgame made another $62 million between its fourth week and final day in theaters domestically. Like Midsommar, though, Endgame also made nearly the total of its revenue within the first 31 days. But $64 million isn’t something to scoff at.

“I do realize that some of our competitors are anxious about this change,” AMC CEO Adam Aron said after inking the Universal deal. “Change is always difficult for some to cope with. We've researched it, we've modeled it, we've thought about it, we've argued about it, we've debated it, and we're sure that we're coming out ahead."

Statistically, fewer people are going to theaters than ever before but they are going for more or less of the same type of movie. This isn’t a subjective dig at any one type of film — but statistically, a family of four is more likely to spend an outing at the movies watching something like The Croods: New Age or Guardians of the Galaxy than Nomadland. This doesn’t mean Nomadland shouldn’t play in theaters — there is an audience of filmgoers, especially in cities like New York City, Los Angeles, Chicago, San Francisco, Seattle, Austin, etc who want to go see Nomadland in an actual theater. There’s just no reason to keep the majority of films in theaters after 30 days.

While box office revenue has mostly increased over the last 25 years, ticket sales have steadily decreased. This is because people are attending movie screenings less on average, but showing up in droves for specific titles. For those titles, being able to remain in theaters for 90 days is crucial for both the studio and the theater chains — you don’t take a $1.5 billion movie out after 30 days of playing. And, for theater chains, it allows new movies to play and potentially bring in more customers than something in its eighth week would.

For literally everything else, having the freedom to determine when to bring it to a streaming platform to push consumers toward a specific product is crucial.

Come for Mission Impossible 7, stay for Criminal Minds

Most streaming services launching now aren’t likely to be profitable for at least another three to five years. That’s if everything works out the way data models predict they will, too.

Take ViacomCBS. The company’s goal is to grow its total streaming revenue to north of $7 billion by 2024, CFO Naveen Chopra announced during the company’s investor presentation. That includes Pluto TV, ViacomCBS’ advertisement supported free streaming service amassing between 100 and 120 million global monthly active users. To try and ensure that revenue is met, ViacomCBS will increase its spend on streaming specific content to $5 billion by 2024. More money could be spent if subscriber growth outpaces ViacomCBS’ goal and, although Chopra didn’t say, I imagine content spending specifically on streaming could potentially slow down if the opposite proves to be true, too.

As we’ve gone over many times in this newsletter, the best way for companies to try and achieve that goal is through a combination of new content that acquires subscribers and a bountiful library that retains their monthly subscriptions. In order to do that, ViacomCBS struck an output and licensing Pay 1 deal with cable network Epix that will give ViacomCBS more control over what movies appear on Paramount+, and how quickly they appear. As Variety reported, “Paramount will be paying Epix to sub-license the older titles and to buy out the pay 1 windows on the franchise titles.” This is on top of moving Paramount films’ Pay 1 windows directly to Paramount+, a benefit of vertical integration.

This is key. It also comes back to the initial point about a shorter theatrical window. Box office revenue isn’t just one equation. There are subsequent windows to take into account. For example, if a studio like Disney signs a Pay 1 deal with HBO or Showtime for movies like Black Widow or Toy Story 4 to play exclusively on those networks for a period of time, the cost of those movies takes into account box office revenue.

In these predetermined deals, Disney and HBO (or WarnerMedia) determine how much the studio is set to receive based on the box office revenue of the films the deal covers. If a movie makes $1 billion at the box office, HBO pays a certain amount ($xxxx). If a movie makes $500 million, HBO pays ($xxx), so on and so forth. The deals don’t cover specific movies, but box office revenue for each film does play into the overall payment. Same rules applied for physical DVD and Blu-ray releases at stores like Walmart at one point in time.

As one former studio executive told me, this is one of the biggest issues with the streaming pivot that teams will have to figure out — when decimating the overall box office revenue, studios are all cutting off all “ancillary revenue.” Let’s think about this in terms of Paramount’s new move — films like Mission Impossible 7 and A Quiet Place II are effectively skipping the Pay 1 window (or moving it) to Paramount+. Instead of earning $xxxx from a Pay 1 partner, ViacomCBS is moving to bring those movies to Paramount+ first.

ViacomCBS is effectively hoping having top titles on Paramount+ sooner than anywhere else bought through the deal will drive subscribers, and the thousands of titles that also come with the Epix deal will keep them there. Taking into account the aforementioned equation, moving the pay 1 window to Paramount+ and having films leave theaters sooner to appear on the streaming service earlier only works if those films bring in a substantial number of subscribers, and then keep them there. This will take years to figure out if it’s working overall, but if overall subscriber gains remain lower than expected for each movie over the next 48 months, that’s a problem.

Double, then triple, then quadruple

Once a streaming service hits two strides, companies like ViacomCBS and WarnerMedia can start making next moves. First is hitting a certain number of subscribers, say between 50 and 75 million. This is just an arbitrary number, but signifies that there’s a substantial number of subscribers who have joined the service for specific content. Second is maintaining a certain level of churn.

Let’s look at Netflix. It took Netflix more than a decade to hit a point where the company won’t have to borrow money anymore, ending a period of debt that saw many analysts uncertain about Netflix’s future. Through the debt Netflix took on, using it for content purchases (coming in at just under $19 billion by 2021) and product features that helped Netflix continuously build its subscriber base, the company built a stable foundation.

Throughout the years, Netflix was able to start introducing incremental price increases because of increasingly consistent, new content from a variety of genres alongside an impressive library and new features that made it easy to use. The foundation remained, so increases could occur. Those price hikes helped improve Netflix’s overall ARPU (average revenue per user) and steadily increase the monthly recurring revenue it was making.

Arguably, this is also why Disney is increasing prices already for Disney+. With nearly 100 million subscribers and less churn than the industry norm (sitting at just under 5%, according to data from Antenna), plus a plethora of new titles on the way, Disney can afford to charge people an extra dollar or two and expect to not lose too many customers.

On that front, there is some good news. Data from Antenna found that in ViacomCBS’ third quarter in 2020, CBS All Access featured the highest annual growth, which was largely driven by a new NFL season and the UEFA Championship League — areas ViacomCBS is leaning into with Paramount+. Showtime also grew 32%, and my assumption is that it's tied to the cheaper bundle once available through Apple. ViacomCBS also plans to continue selling a bundle of sorts, incorporating BET+ (1.5 million subscribers) with Paramount+ and Showtime. No details are available on that now.

At the same time, however, CBS All Access and Showtime were on the higher end of the churn spectrum, coming in either just under or around 10% respectively. To put that into context, Netflix’s churn rate sat at roughly 3%, according to Antenna. One theory seems to be that having an array of new films will help bring subscribers into Paramount+, and the ViacomCBS combined library will keep them — even after the movie finishes playing or the NFL season comes to an end.

That’s certainly a possibility, but Paramount isn’t Disney. It’s not Fox or Sony or Warner Bros. In 2019, Paramount brought in $1.35 billion globally. This represents just 4.6% of the international market share. In comparison, Disney/Fox brought in a combined $13.15 billion (51.54%), Warner Bros. brought in $4.4 billion (16.65%), Universal brought in $3.67 billion (12.57%), and Sony brought in $3.35 billion (11.71%). Will Paramount’s films bring in enough subscribers after those movies leave theaters, even just after 45 days? Mission Impossible 7 and A Quiet Place II are not exactly Star Wars, Wonder Woman 1984, or The Matrix 4.

Remember, the streaming bet seems like a necessity at each company but sacrificing the pay 1 windows, more than anything else, and all the ancillary revenue is a lot of money to make up for, as one executive told me. It’s a dramatic change to the system, they added. Companies like Disney are still figuring it out, and they’ve got a brand, product, and subscriber base that ViacomCBS doesn’t.

If those films can’t bring in substantial subscriber gains, and the long play model isn’t going to generate the type of subscriber growth needed for increasing monthly recurring revenue at a higher ARPU, then the best bet is returning to the model that does work for ViacomCBS — licensing.

Licensing is a necessity, but a double edged sword

ViacomCBS generates significant revenue licensing its content. Analyst Robert Fishman at MoffettNathanson specifically wrote in a new note that “ViacomCBS generated $6 billion in content licensing” in 2020. But, “given the company’s plans to self-license, it remains unclear what impact this will have to third-party licensing revenue.”

Part of that revenue came from selling off titles during the height of the pandemic due to come out in 2020. CBS All Access and Showtime weren’t big enough to dump the films on, so they got sold off while ViacomCBS tried to decrease its losses. The Trial of the Chicago 7 went to Netflix for a reported $56 million. The Lovebirds also went to Netflix for somewhere in the “high-$20 million/low-$30 million range,” according to The Wrap. Coming 2 America was sold to Amazon for a reported $125 million. Paramount kept itself going by selling off notable titles, but this isn’t a new strategy. The studio has a multi-picture deal with Netflix, and CEO Bob Bakish told analysts the plan is still to license series and films out to effectively help pay for everything.

“Content licensing is an important business but … our strategy is clearly evolving, particularly with Paramount+,” Bakish said during an earnings call, as reported by Deadline. “We can’t keep all that for ourselves. It doesn’t make sense. It’s too much,” he said.

Licensing is a quick and effective way to generate revenue, but it also assuredly drives people toward other streaming platforms owned by companies with similar strategies. They have libraries and new films for people to watch, too. Trying to pre-determine what’s valuable and what isn’t can sometimes require a prophet. Yellowstone, for example, is one of cable’s biggest shows. ViacomCBS owns it, but the show is playing exclusively on Peacock. ViacomCBS is hoping to bring an audience over with a new Yellowstone universe (one that includes a massive deal for creator Taylor Sheridan), but Peacock is benefitting from Yellowstone now. Same with Emily in Paris or Coming 2 America for Netflix and Amazon.

If a bunch of Paramount movies (and ViacomCBS shows) are spread out to all the different streaming services, it takes longer to remind people what Paramount+ is. This isn’t just a ViacomCBS or Paramount+ problem; NBCUniversal and WarnerMedia license its content as well because of revenue importance. As they move away from investing in linear offerings or trying to move linear programming into OTT spaces, (this is also why the ad-supported cheaper tier is key, especially with more addressable TV advertising (DAI) entering the market), balancing incoming revenue with necessary operation and content costs to build streaming platforms is key. Hence: licensing.

On the opposite side is Disney. Eventually, the marketing cost of acquisition will be even lower because Disney+ will become synonymous for exclusive access to a certain type of globally recognized brand or franchise. Less marketing is needed to bring subscribers in. The ball picks up steam as it rolls.

That kind of brand recognition and synonymity with content isn’t there on Paramount+. Its movies are also not “brand” heavy. Mission Impossible 7, A Quiet Place 2, Spongebob Movie: Sponge on the Run, and No Time To Die are all notable independent features, but I doubt the vast majority of consumers would know to group them all under Paramount or ViacomCBS. So, the cost of marketing acquisition remains high for a period of time. People need to be reminded all of these things are on Paramount+. Shortening that time frame by moving films faster to Paramount+ might help, but that’s still a lengthy process.

All of which is an incredibly long way of saying that many of these streaming services are built on the idea of potential. There’s the potential that films bring in subscribers, and potential for homes to have up to five streaming services, and the potential that Paramount+ creates an undeniable hit or boasts the best library that it succeeds. Undeniably, linear television feels like a relic of the past as everyone all but abandons pay TV. The theatrical window is forever changed. It feels like so much of the foundation that kept Hollywood working for years is crumbling as new buildings are erected. It’s just determining where companies best fit in the new mold.

Not everyone has to be a content provider and a distributor.